Aug 12, 2016 | Branded Content and Social Business, Connecting with Customers, Culture & Leadership, Customer Experience & Insights, Emerging Trends, Futureproofing & Disruption, Leading Winning Business, Marketing & Brand Engagement, New Business Models & Strategies, Product & Service Innovation, Startups & Accelerators, Technology & New Media, The Crowd, Sharing and On-Demand Economy, WHAT'S NEW

Having looked at more than a hundred digital transformation models, one of the common frustraters I find is that each model seems very tribal.

CIOs author transformation models focused on technology and the inherent issues of integration, platforms, security, features and compliance with passing reference to end users and business leadership.

CMOs author transformation models focused on acquiring and retaining customers talking up customer experience, new media, content/inbound marketing, tracking performance and revenue acquisition with passing reference to issues concerning the organizational change, integration, risk management and technology architecture and execution.

And yet another party – CEOs/COOs author transformation models focused on how to generate competitive positionings, cost and workplace efficiencies, strategic alignment, culture change and organizational speed and delivery with passing reference to functional-specific issues related to technology, marketing, HR, sales and finance.

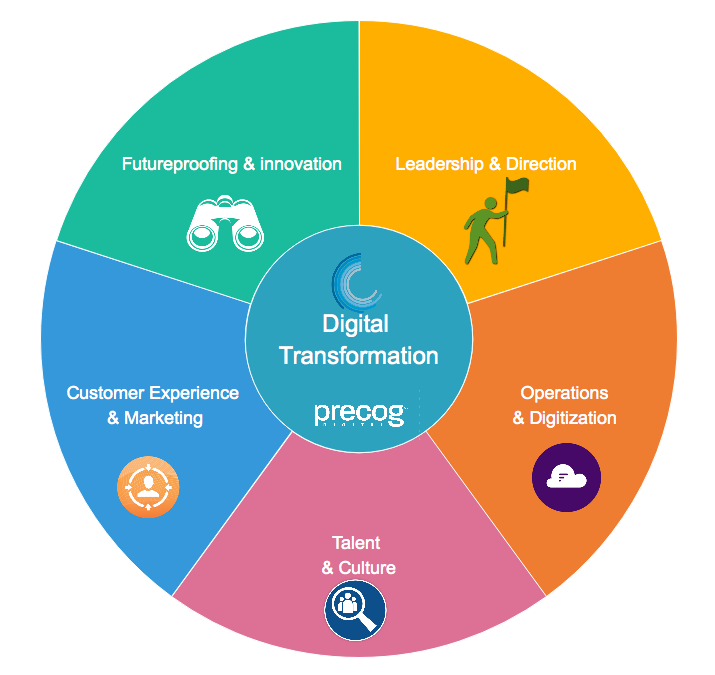

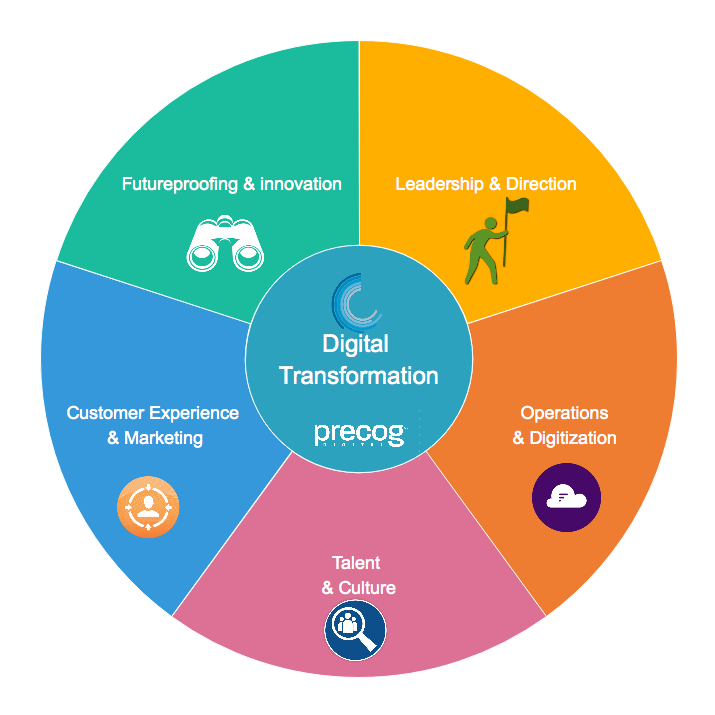

All of these are incomplete. True digital transformation embeds itself deeply in organizations and changes the culture, behaviours, strategies and tactics of the business, customer-facing, talent leading and technology managing facets of the business.

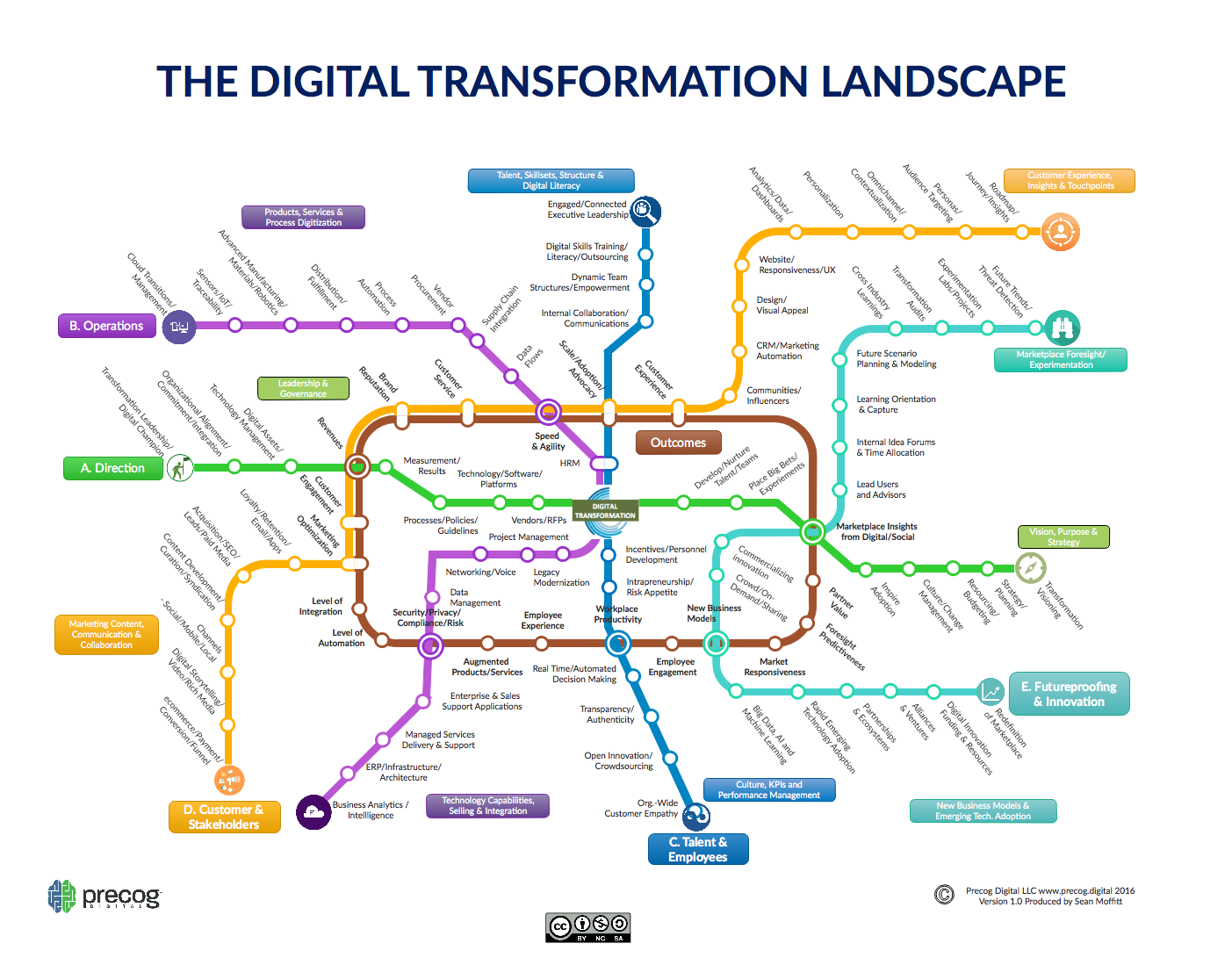

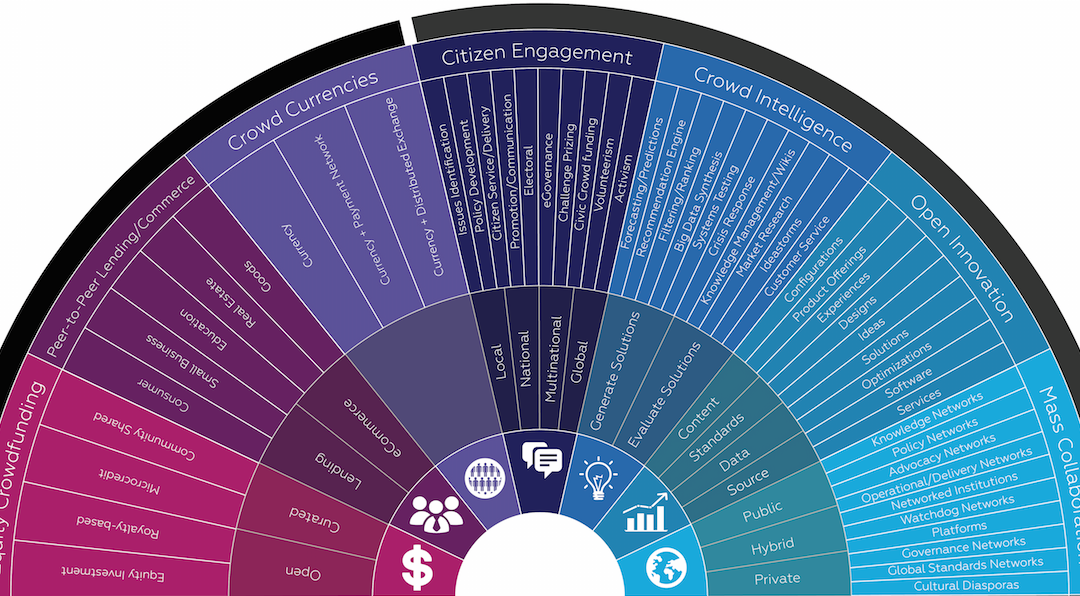

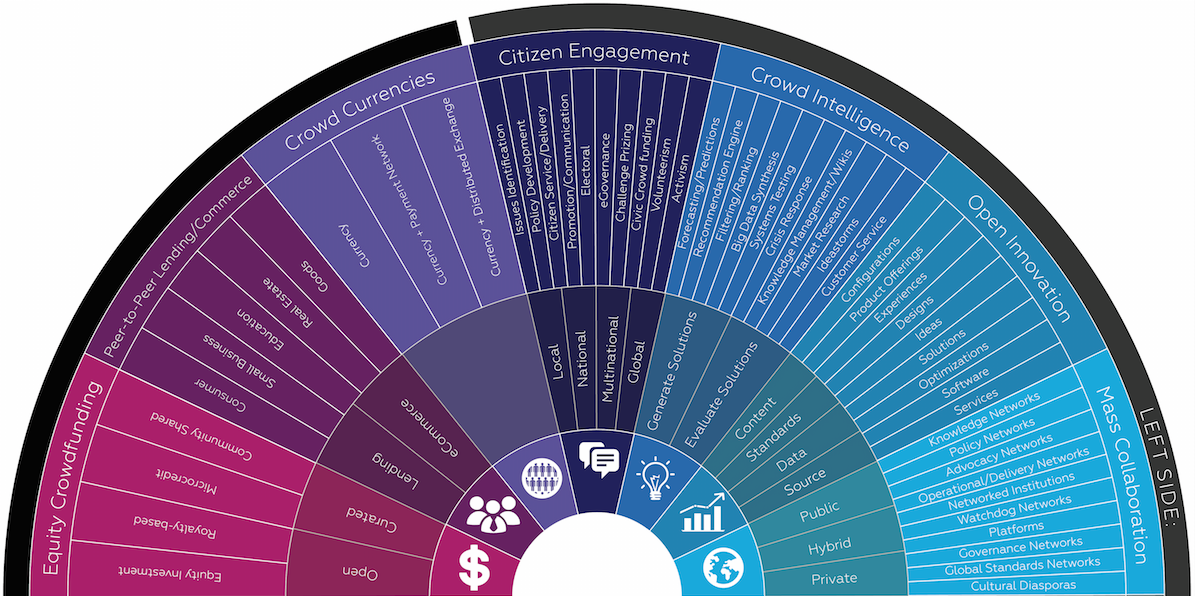

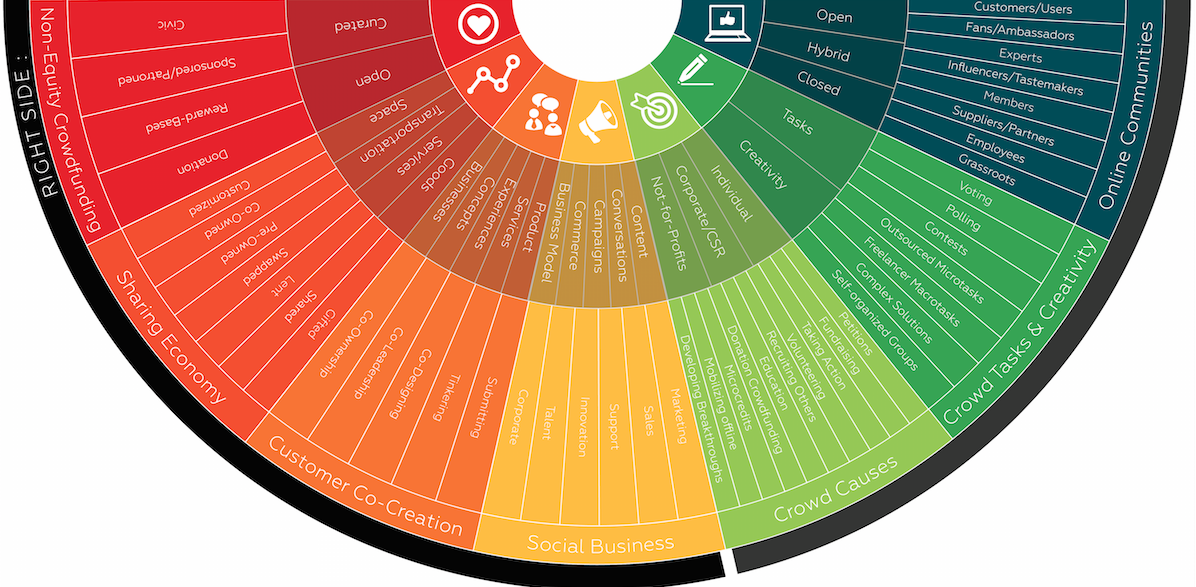

We’ve attempted to build a more holistic model – including the key 5 transformation segments, 10 sub-segments, 20 expected outcomes and 90 sub-areas of transformation concern. Let us know what you think and if we have missed anything.

Attached is a higher definition PDF to search all the intricacies of our new model digitaltransformationlandscapeprecog

Jul 26, 2016 | Connecting with Customers, Culture & Leadership, Futureproofing & Disruption, Leading Winning Business, Technology & New Media, WHAT'S NEW

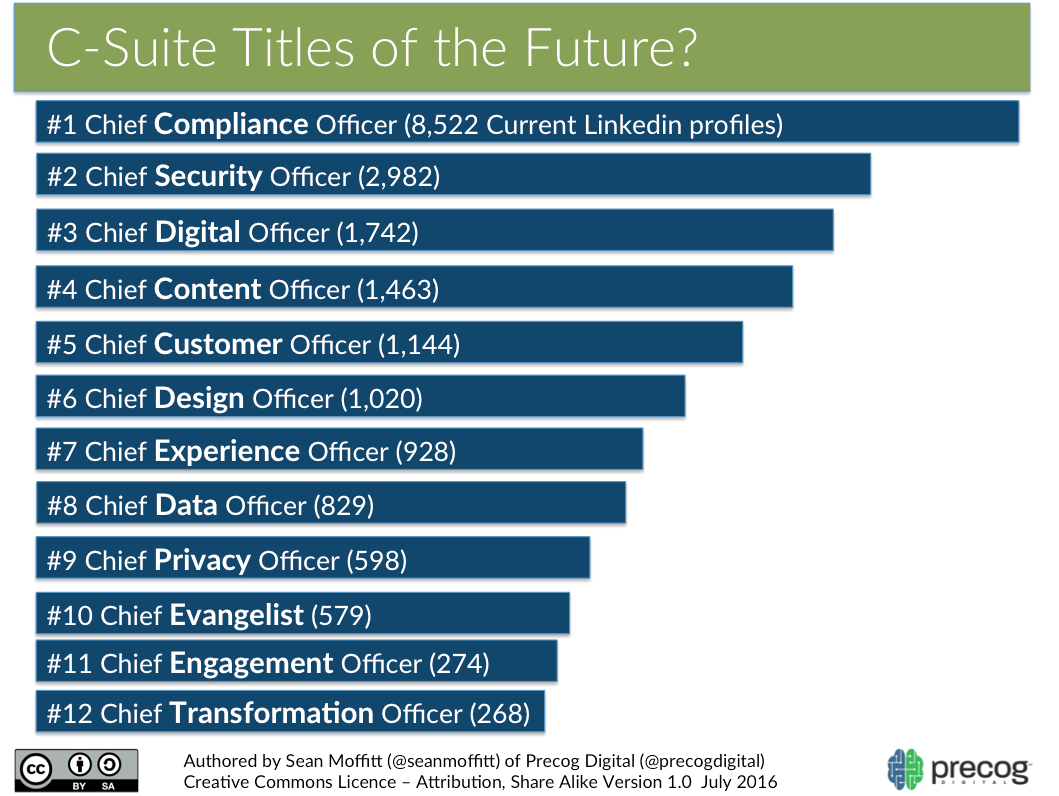

Ask any CEO and they will tell you that leading a business is more difficult than it has ever been with more people and topics vying for your attention. A number of relatively new tribes of professionals are asking for their fair share of resources and management credibility, who shall wear the next C-suite crown?

Get past the top 7 (CEO – chief executive officer, COO – chief operating officer, CMO – chief marketing officer, CFO – chief finance officer, CHRO – chief human resources officer, CTO/CIO – chief technology/information officer and CSO – chief sales/business development officer – sorry Chief Strategy Officer and Chief Investment Officer, you just missed the list) and the now the question is – “will a changing business landscape and disruption create opportunity for more executive level roles?”

Attached (above) are 12 roles that may be candidates for the crown. If you group them into clusters, they fall into 4 camps of executive level of talent:

Risk Security Focus – #1 Chief Compliance Officer, #2 Chief Security Officer (note: these two also overlapped with popular Chief Risk Officer) and #9 Chief Privacy Officer are focused on the legal, regulatory, privacy, security, risk management and disaster recovery demands and stewardship for the business in an increasingly complex age where threats might not be seen or forecast.

Customer Experience Focus – #5 Chief Customer Officer, #6 Chief Design Officer, #7 Chief Experience Officer, #10 Chief Evangelist and #11 Chief Engagement Officer underscore the need to get closer and understand customers at a strategic level.

Digital Focus – #3 Chief Digital Officer, #4 Chief Content Officer and #8 Chief Data Officer point to a need for business to get more sophisticated about technology at an executive level with the explosion of technologies, digital media and sources of information and data sources now available.

Business Change Focus – creeping in at the bottom of the list is #12 Chief Transformation Officer – suggesting that the imperatives for business are so great that they need to move beyond a specific function and instead be spearheaded by a centralizing focus.

So what do you think? Who will be next? Which will have the lasting power to stick around? Is there a better new way to the C-Suite than these 12, let me know.

May 24, 2016 | Branded Content and Social Business, Connecting with Customers, Culture & Leadership, Customer Experience & Insights, Digiball - Sports & Technology, Emerging Trends, Front Page, Futureproofing & Disruption, Hot Topics, Leading Winning Business, Marketing & Brand Engagement, New Business Models & Strategies, Product & Service Innovation, Social Innovation & Transforming Better Worlds, Startups & Accelerators, Technology & New Media, The Crowd, Sharing and On-Demand Economy, WHAT'S NEW

As part of a personal and new economy manifesto, I have been compiling the best examples of a society, culture, business and technology that keeps getting sped up. It’s one thing to say it as a “throwaway line”, it’s another thing all together to find the evidence. I’ve been foolish enough to chase down various sources and work my way backward into history and forward into the future.

Here is my first initial instalment of 5 posts (x 6 examples) that point to a world that keeps getting quicker, faster and tougher to evaluate. These snippets once again prove that whereas “we may overestimate the change that is happening in the short term, we massively underestimate how much is changing in the near/long term.”

The key takeaways – embrace change, don’t get stuck on one paradigm, experiment and fail/scale quickly and become a daily, life-long learner looking at what’s changing constantly.

Here are the first ones…enjoy:

Fast Forward #1 – The Time We Spend on Digital Each Day (2008-2017)– yes it’s more than doubled over the last decade.

Fast Forward #2 – Digital Video The World Consumes Each Month (2008-2016) – and let’s just say PB = a petabyte which is a lot

Fast Forward #3 – The Number of Digital Devices We Connect To (2003-2020) – and since 6.6 is the average, many of us will have 30+ devices connected to us.

Fast Forward #4 – The Amount of Olympic Tweeting (from Beijing to London to Rio) – yes despite Twitter stagnation, this will be a social Citius, Altius, Fortius this summer

Fast Forward #5 – Global Social Network Audience (2007-2019) – in 12 years, we will have almost septupled the audience connected on social platforms

Fast Forward #6 – Global Internet Users (2002-2020) – our world keeps getting smaller and smaller

Follow or link to me for more Fast Forward Updates here, my website SeanMoffitt.com and a new eponymous venture launching soon.

Apr 11, 2016 | Branded Content and Social Business, Connecting with Customers, Culture & Leadership, Emerging Trends, Front Page, Marketing & Brand Engagement

In association with Wikibrands and our upcoming presentation “Personal Branding in a Snapchat Age“, we are fielding our first survey pulse check on the role of Personal Branding.

Most of my history has focused on how corporations, startups and organizations have built and incubated their brands, we’re wondering of the same rules hold for personal brands.

So in this survey, we’re asking:

- How important is personal branding? and has it increased in importance?

- Are you even comfortable with the term “Personal Branding”?

- Do employers care about the value of your personal brands?

- Are you currently happy with your own personal brand?

- Top reasons to invest in your personal brand?

- Top positions/functions that can benefit from a strong personal brand?

- Key Personal Branding Success Factors?

- Key Personal Branding Media/Content Tools?

- Top Personal Branding Social Media Platforms/Tools?

- Most frowned-upon aspects of Personal Branding?

- in your opinion, the greatest and most horrible personal brands?

- What forces will drive personal brands in the future?

- What are the best habits of great personal branders?

We’ve had some great answers already, and we’d love your thoughts. Hopefully you can grab 5-10 minutes and provide your insight. We will recognize and share toppling results with all respondents.

Additionally, if you’re considering any type of content or event around personal branding, we are expecting results finalized at the end of April’16 and would love to collaborate. Please get in touch with us here.

Apr 1, 2016 | Connecting with Customers, Emerging Trends

Mar 31, 2016 | Branded Content and Social Business, Connecting with Customers, Culture & Leadership, Customer Experience & Insights, Emerging Trends, Marketing & Brand Engagement

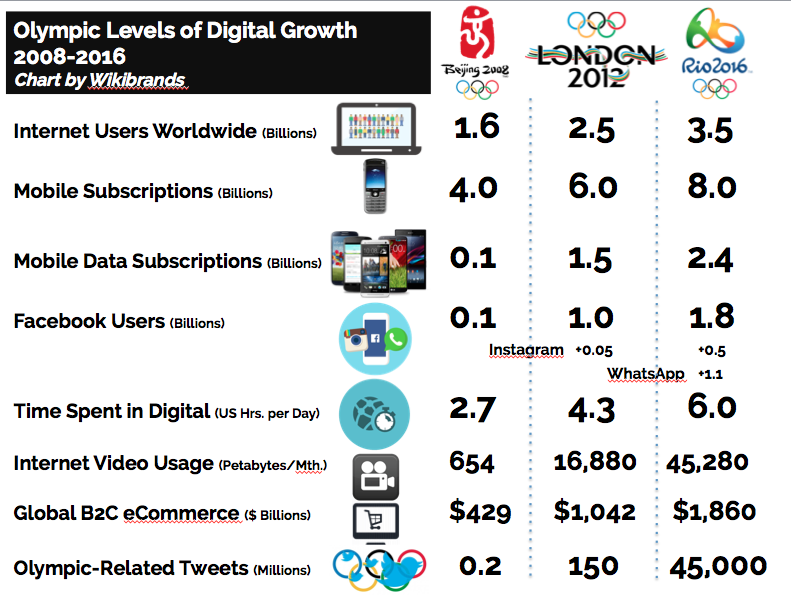

In a world that is all about “what happened two minutes ago”, the Olympics represent a once-every-four-year touchstone on what really has changed in the world.

Although Beijing 2008 (remember that crazy lit-up swimming pool) and London 2012 (I seem to recall sprinter Usain Bolt’s successful defence and Danny Boyle’s impressive opening ceremony) are faded memories, they are 1461-day mileposts in many sporting fields. I thought i would reprise an analysis I did back in 2012 and look at what Olympian levels of change have happened over the last 8 years in the technology track and digital field.

Sources- Internet Live Stats, Cisco, Counterpoint Stats, Statista, Facebook, Twitter, Ericsson, ATOS

We looked at 8 different statistical weather vanes that we think best represent the state of growth in the digital universe.

- Internet Users Worldwide Growth

The growth in interest users is reaching a tipping point as they will represent close to half the world’s population (~46%) in 2016, and double what tit was 8 years ago. That’s pretty hefty given that the internet universe was a precocious 1% of the world’s population back in 1995. It will be interesting to see the trajectory of the internet and what companies focus on as internet population growth has slowed on an annual basis from 14.7% in 2008 to 7.5% in 2016. Will be still care about the developing worlds and getting the next 3-4 billion online through balloons, drones, cheaper devices and free internet? Or will we consider squeezing that juice out of the orange too hard and focus instead on enhancing the web for people already attached and drive better experiences and for companies the nirvana ARPU (average revenue per user)?

2. Mobile Subscriptions

2015 represented an interesting year for mobile in that there are now more mobile subscriptions than there are people in the world. That doesn’t mean everybody is connected, some of us have more than one way to connect (about 1.47 subscriptions per connected user). But we are reaching saturation point. The growth engine may be in connected devices. When we include the internet of Things and connected homes, cars, wearable and TVs. it is expected we will move 1 connected device per person in 2008, to 2 in 2012, to 4 in 2016 and nearly 7 in 2020.

Some interesting prospects exist in developing world nation where in places like Kenya the majority of the population owns a mobile phone to perform life’s essential services even though only 25% own a physical, real venue bank account.

3. Mobile Data Subscriptions

Taking a global view, we have barely scratched the surface on what we can do with the smarter version of mobile – location aware, personal sensing, app-driven smartphones. Although we have experienced 24X growth over the last 8 years of more sophisticated smartphones and mobile PCs, that will be another 2.5X growth over the next 4 years. And it’s not only the number of people, but it’s also what we’re doing on our devices, enhanced need for data-rich infrastructure and our growing dependence on them.

4. Facebook Users

Facebook had barely emerged from Mark Zuckerberg’s Harvard dorm room and in the shadow on ill-fated MySpace back in 2008. In fact, you couldn’t even Like things on Facebook until 2009. By summer 2016, It will have experienced 19X growth between the Beijing games and the Rio ones. It is less a social website now and more social ecosystem with flanges all over the place, competing against Google, Apple and Amazon for your life needs. And just when you thought, Facebook could lose its way and maybe become irrelevant, they decided to gobble up and grow billions of other new people and connections on platforms like Instagram which is bought in 2012 and WhatsApp in 2014, never mind it’s investment with millions of other users on a standalone FB Messenger and now Oculus Rift in 2016.

5. Time Spent in Digital

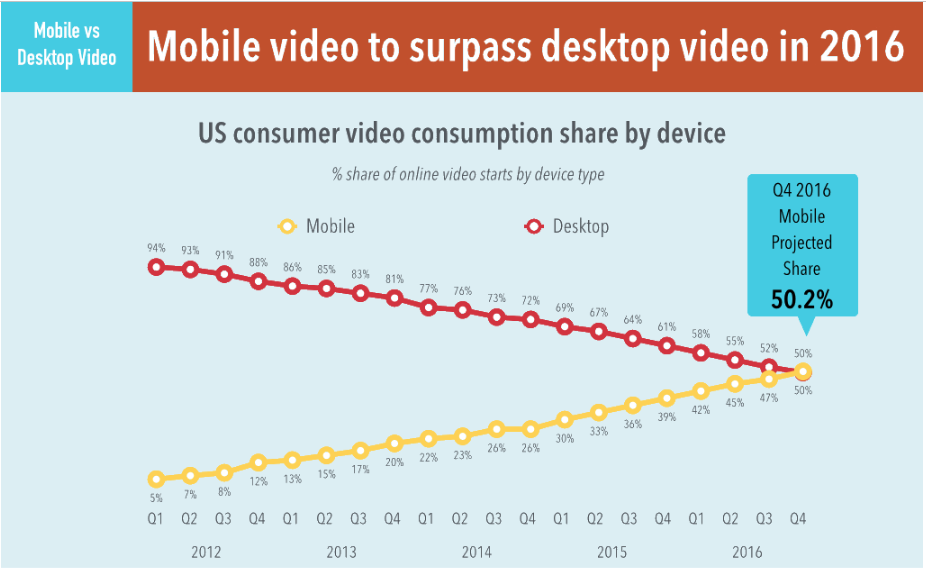

Much to family, classroom and company discord, we are slowly becoming addicted to devices. The US media consumption trend reflects the world more broadly with our inability to stay away form our screens. When watching the Olympics in Rio, we will spend 2.3X more time per day in digital media then we did while watching Beijing – that;’s about 6 hours each day!. And we will do it anywhere. Back in 2008, we spent 11% of our digital time in mobile, now we will be spending 50-60% of our digital time in mobile. Remember when addictions were smoking, gaming or sole a young people arena? Think again.

6. Video Usage

We will be watching 69X more video than we did in Beijing 8 years ago. That’s more Netflix. That’s more Facebook Video. More YouTube. More Meerkat/Periscope. And I’m sure a tonne of other niche video channels. Fully 60% of internet traffic will be video this year. And mobile video views are up a whopping 844% since 2012. the desktop is becoming less and less relevant for even the bandwidth hogger – video – in 2016.

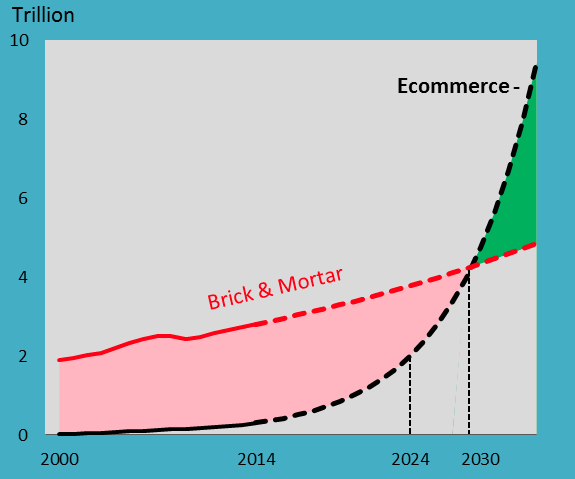

7. eCommerce/mCommerce

There is 4.3X more stuff being bought online in 2016 then 8 years ago. That may seem like a disappointment vs. other parts of the burgeoning web, but it does factor in the slower adoption of customers due to a variety of factors – preference of brick and mortar, trust/security issues, quickness of fulfillment/delivery/returns obstacles and spotty customer service. As internet commerce retailers figure this out, you will see a longer term tipping point. As US brick and mortar commerce is growing at 2.8% and internet-enabled commerce growing at 18.7% annually, we will see those two lines cross by 2030 – only 3 more Olympics away.

8. Olympic-Sized tweets

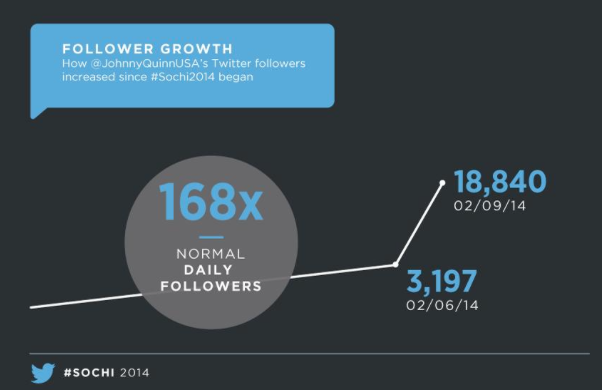

A full forensics on digital growth wouldn’t be complete without speaking to the amount of Tweets this summer we’ll peruse about the Rio Olympics. As much as Twitter has had its well publicized struggles on user and revenue growth, there will be 225,000X more tweets about #Rio2016 than there was about Beijing. Part of that is a function of the fact there were only 6 million users and only a handful of athletes back in 2008, 150 million in 2012 and now 350 million estimated Tweeters in 2016. Heck the hashtag wasn’t even invented until 2007! As can be seen by American bobsledder’s Johnny Quinn’s gold medal Sochi twitter performance, niche athlete can become front page headline if you play your cards and tweets right. they will all be on in 2016.